Who We Are & What Drives Us

LifeTools Financial

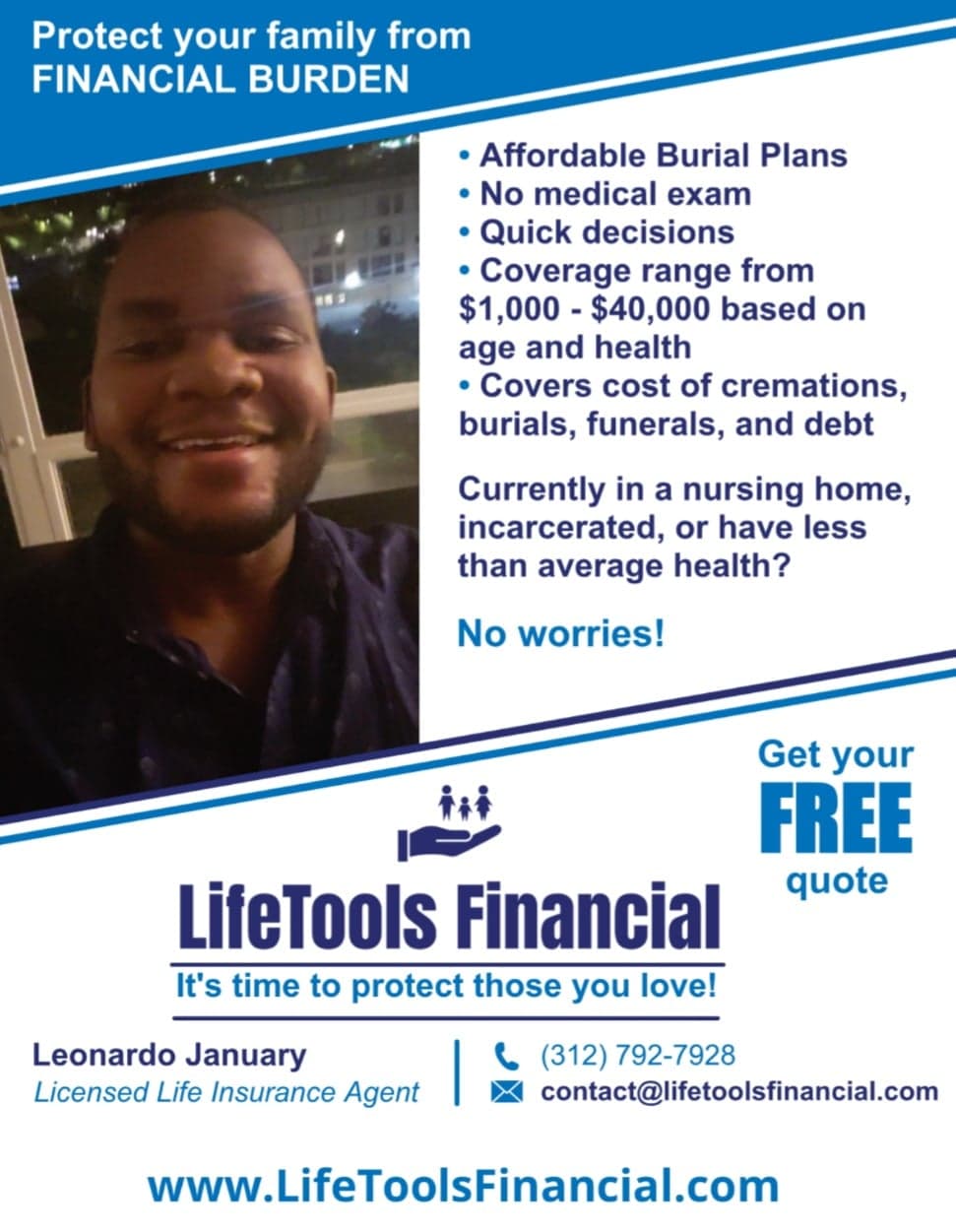

GET AN AGENT WHO CARES!

Leonardo January is a licensed independent life insurance agent and founder of LifeTools Financial. His agency serves clients across the United States and provides them with access to affordable burial insurance, despite health or income.

Please click HERE fill out the required form to receive your quote. After you submit this form, you will be prompted to schedule time on my calendar.

We look forward to serving you!

(312) 792-7928

DON’T WAIT! SPEAK WITH ME TO GET YOUR AFFAIRS IN ORDER AND GET THE PEACE OF MIND THAT YOU DESERVE!

Life Insurance

PROTECT THE ONES YOU LOVE THE MOST

What is Life Insurance

Life insurance is a contract between an insurer and a policyholder. A life insurance policy guarantees the insurer pays a sum of money to named beneficiaries when the insured policyholder dies, in exchange for the premiums paid by the policyholder during their lifetime.

How Life Insurance Works

A life insurance policy can has two main components - a death benefit and a premium. Term life insurance has these two components, but permanent or whole life insurance policies also have a cash value component.

- Death Benefit – The death benefit or face value is the amount of money the insurance company guarantees to the beneficiaries identified in the policy when the insured dies. The insured might be a parent, and the beneficiaries might be their children, for example. The insured will choose the desired death benefit amount based on the beneficiaries’ estimated future needs. The insurance company will determine whether there is an insurable interest and if the proposed insured qualifies for the coverage based on the company’s underwriting requirements related to age, health, and any hazardous activities in which the proposed insured participates.2

- Premium – Premiums are the money the policyholder pays for insurance. The insurer must pay the death benefit when the insured dies if the policyholder pays the premiums as required, and premiums are determined in part by how likely it is that the insurer will have to pay the policy’s death benefit based on the insured’s life expectancy. Factors that influence life expectancy include the insured’s age, gender, medical history, occupational hazards, and high-risk hobbies. Part of the premium also goes toward the insurance company’s operating expenses. Premiums are higher on policies with larger death benefits, individuals who are higher risk, and permanent policies that accumulate cash value.

- Cash Value – The cash value of permanent life insurance serves two purposes. It is a savings account that the policyholder can use during the life of the insured; the cash accumulates on a tax-deferred basis. Some policies may have restrictions on withdrawals depending on how the money is to be used. For example, the policyholder might take out a loan against the policy’s cash value and have to pay interest on the loan principal. The policyholder can also use the cash value to pay premiums or purchase additional insurance. The cash value is a living benefit that remains with the insurance company when the insured dies. Any outstanding loans against the cash value will reduce the policy’s death benefit.

Types of Life Insurance

Many different types of life insurance are available to meet all sorts of needs and preferences.

- Death Benefit – The death benefit or face value is the amount of money the insurance company guarantees to the beneficiaries identified in the policy when the insured dies. The insured might be a parent, and the beneficiaries might be their children, for example. The insured will choose the desired death benefit amount based on the beneficiaries’ estimated future needs. The insurance company will determine whether there is an insurable interest and if the proposed insured qualifies for the coverage based on the company’s underwriting requirements related to age, health, and any hazardous activities in which the proposed insured participates.

- Premium – Premiums are the money the policyholder pays for insurance. The insurer must pay the death benefit when the insured dies if the policyholder pays the premiums as required, and premiums are determined in part by how likely it is that the insurer will have to pay the policy’s death benefit based on the insured’s life expectancy. Factors that influence life expectancy include the insured’s age, gender, medical history, occupational hazards, and high-risk hobbies. Part of the premium also goes toward the insurance company’s operating expenses. Premiums are higher on policies with larger death benefits, individuals who are higher risk, and permanent policies that accumulate cash value.

- Cash Value – The cash value of permanent life insurance serves two purposes. It is a savings account that the policyholder can use during the life of the insured; the cash accumulates on a tax-deferred basis. Some policies may have restrictions on withdrawals depending on how the money is to be used. For example, the policyholder might take out a loan against the policy’s cash value and have to pay interest on the loan principal. The policyholder can also use the cash value to pay premiums or purchase additional insurance. The cash value is a living benefit that remains with the insurance company when the insured dies. Any outstanding loans against the cash value will reduce the policy’s death benefit.